Why Make Pension Contributions?

Many Pensions might seem like a maze of rules and jargon, but at their core, the concept is straightforward. Sure, the State Pension is there to help, but, as we’ve covered previously, it’s not going to fund your dreams of traveling the world, spoiling the grandkids, or simply enjoying a comfortable retirement.

So, while it might seem like a lot to wrap your head around, taking the time to understand the benefits of saving into a pension scheme could be one of the smartest financial decisions you ever make.

In this video, we'll break down the essentials of pension contributions, covering both personal and employer contributions. We’ll also explain how these contributions can significantly reduce your personal tax bill. And if you’re a business owner, stay tuned because pension contributions can also help lower your corporation tax liability. By the end of this video, you’ll have a clear understanding of why making pension contributions is one of the most tax-efficient ways to save for your retirement.

What are personal pension contributions?

Let’s start with personal pension contributions. In the UK, personal pensions are a popular way for individuals to save for retirement. These include private pensions like Self-Invested Personal Pensions, or SIPPs, and workplace pensions where you contribute directly from your salary.

When you make a contribution to your pension, your money is invested in various assets, such as shares, bonds, and funds. Over time, the goal is for your investments to grow, building a substantial pot of money that you can draw from in retirement. Most importantly, investments held within your pension wrapper grow free of tax, giving your money a significant boost over time.

One of the key benefits of contributing to a personal pension is the tax relief you receive on contributions. The UK government incentivizes investors by offering tax relief on the contributions you make. This means that a portion of the money you'd normally pay in tax goes into your pension instead. It’s like getting a bonus just for saving for your future.

If you’re a basic rate taxpayer, which means you earn up to £50,270 a year (as of the 2024 tax year), you automatically receive 20% tax relief on your contributions. For example, if you want to contribute £100 to your pension, you only need to pay £80. The government then adds the remaining £20 to your pension. In this instance, the £100, which includes the tax relief, would be referred to as the Gross amount and the £80 would be referred to as the Net amount.

Now, some pension providers list 25% as the additional pension contribution received from the government, rather than the 20%. This is technically true because, to use the previous example, £20 of £80 is 25%. A little sneaky, but the relief on pension contributions still adds up to the same cash amount.

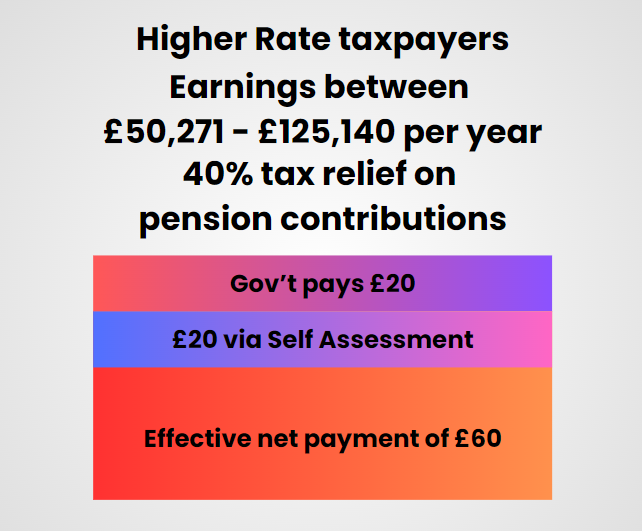

For higher-rate taxpayers—those earning between £50,271 and £125,140—you can claim an additional 20% tax relief, bringing the total tax relief to 40%. Just like with basic rate taxpayers, you contribute £80, the government adds £20, and you can claim another £20 when you complete your self-assessment tax return. So, effectively, a £100 gross contribution only costs you £60.

And for you additional rate taxpayers—those earning over £125,140—the tax relief is even more significant. You can claim up to 45% in total tax relief—20% is added directly to your pension by the government, and you can claim an extra 25% via self-assessment.

How do employer contributions work?

These are contributions made by your employer, or your own company, into your pension pot, and they can be a significant boost to your retirement savings.

Under the UK’s auto-enrolment scheme, employers are required to automatically enroll eligible employees into a workplace pension scheme. Employers must contribute a minimum of 3% of your qualifying earnings, while you contribute a minimum of 5%, bringing the total minimum contribution to 8%.

Employer contributions are incredibly beneficial because they help grow your pension pot without directly effecting or reducing your salary.

Many employers also offer a salary sacrifice scheme, which is an arrangement where you agree to reduce your salary in exchange for an equivalent pension contribution by your employer. We’ve covered this subject in a separate video here. The benefit of this scheme is that you pay less in National Insurance contributions because your salary is lower, and your employer may also pass on their National Insurance savings to your pension.

For example, if you agree to sacrifice £1,000 of your salary, your employer may contribute the full £1,000 into your pension. Plus, both you and your employer will save on National Insurance contributions. This can be a highly efficient way of increasing your pension savings.

If you’re a business owner, you can pay into your own pension from cash held within the business. These contributions are considered an expense for the business and avoid corporation tax. Another great benefit of making contributions in this way is that relevant earnings are not considered, meaning you can move funds from your company to your pension in excess of your earnings. But more on relevant earnings in a bit.

What are the tax benefits of making pension contributions?

One of the biggest advantages of pension contributions is that they reduce your taxable income. Since pension contributions are deducted from your gross income, they lower your overall income on which you are taxed. This is especially beneficial if you're close to a tax threshold. If your earnings push you into higher rate or additional rate income tax brackets, making additional pension contributions could potentially lower your income into a lower tax bracket, thereby reducing the amount of income tax you pay.

If your income exceeds £50,000, you may be subject to the High-Income Child Benefit Charge. However, pension contributions can help you reduce your adjusted net income and avoid or reduce this charge. By making pension contributions, you can keep your income below the threshold and continue receiving full child benefit payments. A win-win situation.

The annual allowance for pension contributions is currently £60,000 (as of the 2024-25 tax year). This is the maximum amount you can contribute to your pension each year without incurring a tax charge. If you exceed this limit, you may be subject to an annual allowance charge, which is effectively your income tax rate.

But here’s where it gets even better: there’s a useful rule called carry forward that allows you to use any unused annual allowance from the previous three tax years. This means you could potentially contribute up to £180,000 in a single tax year if you have sufficient unused allowances and still benefit from tax relief.

What are relevant earnings?

Investors can only make contributions within their relevant earnings with a tax year. Simply put, relevant earnings are the types of income that the government considers when calculating how much you can contribute to your pension and still receive tax relief.

So, what counts as relevant earnings? The main types include:

Salary or wages from your job—whether you’re employed or self-employed.

Bonuses and overtime pay

Income from self-employment

Benefits in kind—some non-cash perks from your employer, like company cars, can also be included.

And rental income if you're a landlord and it’s considered part of a property business income.

However, certain types of income don’t count as relevant earnings, like:

Investment income from things like dividends or interest on savings,

State Pension or other government benefits, and

Income from property if it’s purely passive and not part of a business.

Why does this matter? Because the amount of tax relief you can claim on your pension contributions is directly tied to your relevant earnings. The general rule is that you can contribute up to 100% of your relevant earnings, capped at £60,000 per year (as of the 2024 tax year), and still get tax relief.

For example, if you earn £40,000 in relevant earnings, you can contribute up to £40,000 to your pension and receive tax relief on the full amount.

Understanding what counts as relevant earnings ensures you're making the most of your pension contributions and maximizing the tax relief available to you.

The one caveat to this is pension contributions made via an employer or your business, where relevant earnings don’t count. If you have relevant earnings of less than £60,000, or your available carry-forward allowance, you can make contributions in excess of this if it’s coming from your company or employer.

While contributing to your pension has significant tax benefits, it’s important to be aware of the lifetime allowance, which is the maximum amount you can hold in your pension pot without facing extra tax charges. As of the 2024 tax year, the lifetime allowance has been abolished, and any excess over this threshold will no longer be taxed, meaning it's more attractive to contribute larger sums to your pension.

Get in touch

Do you have a question about pensions? We’re here to make it simple. Leave us a message via the submission form button below, and let’s chat. We’re always happy to help.

No financial decisions should be taken based on the content of this website or associated videos. The guidance contained within this website is subject to the UK regulatory regime and is therefore primarily aimed at viewers in the UK. Always take full individual advice first. Regulations and legislation governing taxation, investments and pensions may change in the future.

The content on this page is accurate as of the 2024-25 tax year.